Artificial intelligence (AI) is currently one of the hottest buzzwords in tech and with good reason. The last few years have seen several innovations and advancements that have previously been solely in the realm of science fiction slowly transform into reality. Rapid progress in AI is arousing fear as well as excitement. How worried should you be?

Dr. Jeremy Kedziora is an award-winning researcher with 17 years of experience in machine learning, Bayesian inference, and game theory. He previously served as director of data science and analytics at Northwestern Mutual, leading machine learning efforts in cybersecurity. At fintech startup Giant Oak, he focused on natural language processing in product development. With a Ph.D. in political science and a B.S. in Chemistry, he also spent 9 years at the CIA, leading R&D in data science and modeling. Dr. Kedziora is now MSOE's first PieperPower Endowed Chair in Artificial Intelligence, helping students develop and advance AI responsibly. Join Lauber Business Partners at the University Club of Milwaukee as we host a discussion with Dr. Kedziora on Tuesday, September 26, 2023, from 4:30 to 6:30 p.m. RSVP by emailing Chris De Villers (chris.devillers@lauber-partners.com) using the button below.

5 Comments

Recruitment costs are sky-high. Employers are turning to overseas talent. Employees are being more selective in the roles they take. How can you avoid the harmful situations facing HR departments as much as possible? It starts with eliminating regrettable turnover. Turnover or attrition, or the gradual diminishment of a workforce's size, is a common aspect of any business. Regrettable attrition, however, is when employees who you’d have liked to stay in your organization leave and can be quite alarming. Crucially, regrettable attrition has a negative impact on your team. This is in direct contrast to non-regrettable attrition when it’s a net-positive that an employee left, whether that’s due to their performance or the liability they posed to your business. The impact of regrettable attrition is difficult to assess until it happens, at which point it can already have had a significant, negative impact on your business. Therefore, it’s essential businesses are aware of what causes regrettable attrition, the role culture plays in preventing regrettable attrition, and how to begin addressing it. In this article, we’ll explore each of those pieces of the regrettable-attrition puzzle. Let’s get started. A Smart Team Compared to a Healthy TeamWe often see regrettable attrition in highly intelligent teams. Despite these teams’ abundance of technical skill, they often overlook the importance of a healthy culture. These teams prioritize the ‘smart’ side of their business, but neglect factors that will make their organization ‘healthy,’ such as fostering a stronger work-life balance and building a healthy supportive environment. The result is that valuable team members leave in search of a healthier team and more positive atmosphere. Some of the consequences of that regrettable attrition include:

Organizations need to keep in mind that skills aren’t the only things that matter at work. They should prioritize a healthy team culture in addition to measurable skills. By doing so, organizations can retain talent, enhance team performance, and ultimately achieve greater success. Culture is Essential for Preventing Regrettable AttritionBefore you write ‘culture’ off as another tired corporate buzzword, consider the best team on which you’ve ever worked. What comes to mind right away? It’s probably the people you worked with, and the joy they brought to the role. People and culture—not skills—are what keep employees engaged. While hard skills are necessary for the success of any business, a healthy culture is essential for sustaining that success. Think of the front and back wheels of a bike: your business’ skills—the back wheel—drives you forward, and your front wheel—your culture—keeps you moving in the right direction, avoiding hazards as they arise. So, how does culture impact your organization’s retention efforts?

By focusing on a healthy business culture, organizations can prevent regrettable attrition, increase loyalty, and foster long-term success. The Common Causes of Regrettable AttritionRegrettable attrition often results from poor work-life balance and burnout. Organizations should prioritize initiatives that promote balance, provide stress management resources, and foster a supportive culture for employee well-being. So what drives employees to the point where they feel like they have no choice but to leave? A multitude of factors could be at play, but three that we commonly see include:

Let’s take a deeper look at how these factors become the main drivers of regrettable attrition. Ineffective Communication Can Create ToxicityIneffective communication and a lack of transparency within an organization are massive contributors to regrettable attrition. When communication is needlessly secretive and siloed, it can create an environment of uncertainty and frustration for employees. This lack of clarity creates a breeding ground for misunderstandings, rumors, and ultimately the sense of being disconnected from the organization's decision-making processes. Comparatively, organizations that prioritize transparent communication create an atmosphere of trust and engagement. When a business is open about its goals, strategies, and performance, employees have a clearer understanding of the direction and expectations. Additionally, they can see how their individual contributions align with the organization's objectives, which increases their sense of purpose and motivation. By establishing platforms for dialogue and feedback, employees feel empowered and valued. What’s more, a transparent communication style allows for the efficient exchange of ideas, concerns, and suggestions. Not only can this foster a sense of collaboration and shared ownership, but it can lead to breakthrough ideas that otherwise would have never seen the light of day. If Employees Aren’t Growing, They’re LeavingBusinesses love quotes like ‘if you’re not growing, you’re dying.’ It’s the type of aphorism that you can find hanging from the walls in businesses across the country. While such sayings are a motivator for businesses, they also resonate with talent. If an employee isn’t seeing the opportunity for growth, why would they bother staying around? The truth is that employees who job-hop tend to out-earn their peers who stay loyal to an organization over time. What’s that mean for your organization? That your employees need to be convinced that they are going to grow so much with your organization that it will be more valuable to stay than leave for what could be a significant increase in pay. Investing in training, mentorship, and career development programs is crucial to support employee growth, satisfaction, and retention. By providing opportunities for learning and skill enhancement, organizations empower employees to expand their knowledge, acquire new competencies, and take on more challenging roles. These initiatives not only contribute to personal and professional growth but also demonstrate your organization's commitment to investing in its employees' long-term success. Your Employees Must Be On-Board With Your Organization’s GoalsRegrettable attrition ultimately comes down to relationships, and to understand why employees leave, it’s helpful to consider relationships outside work. Why do friends grow distant? One reason that repeatedly appears is that they want different things from life. The same can be said for businesses and their employees. If your employees aren’t aligned with your organization’s values and goals, it can drive regrettable attrition. To address this, it’s critical that organizations clearly communicate their values and ensure that employees understand and internalize them. This is because when employees feel that their own beliefs align with the goals and values of your organization, they’re more likely to feel a greater sense of connection to their work and less likely to jump ship. Dysfunctional Team Dynamics Lead to DissatisfactionTeams are composed of unique individuals. Humans are complicated. Excellent teams have diversity of thoughts, styles and preferences. This sort of diversity can cause friction within a team. Unless team members understand one another well, communications can be misinterpreted, which can lead to friction within the team, which can lead to division. Individuals have different ways of thinking, communicating and interacting. Many times what one team member thinks is a perfectly acceptable way to communicate may cause another team member to withdraw or maybe become more assertive. If team members can understand each other’s personality, communication preferences and means of thinking, it can go a long way to eliminating miscommunications and team dysfunction. Building this understanding within the team along with clear team expectations, lead to healthy effective teams. Investing in teams to build this type of understanding will lead to extremely effective teams and better organizational performance. Well-regarded management gurus believe high performing teams is one of the most lasting competitive advantages an organization can have. Strategies for Eliminating Regrettable AttritionRegrettable attrition and the factors that cause it aren’t some pesky bug—they can’t be eliminated overnight. There’s no single solution, and finding the answer for your business can take time. That said, the benefits of eliminating regrettable attrition and improving employee retention are huge—even too large to measure in some cases. The truth is that when you lose a valuable member of your team, you’ll never know what could have been. It’s important to prioritize your employees’ well-being and promote a healthy work-life balance, but starting somewhere more concrete will lead to better results. Before you dive into ‘prioritizing your employee’s well-being’ or ‘promoting a healthy work-life balance,’ dig deeper. Start by taking a close look at the factors that enable you to truly improve well-being and a work-life relationship.

By implementing these strategies and emphasizing the importance of communication, growth, aligned values and goals, and enhanced team dynamics you can significantly reduce regrettable attrition’s impact on your business. Lauber Business Partners Can Help You Reduce Regrettable AttritionRegrettable attrition is one of many battles within business. While it may seem like an internal struggle, the truth is that it has everything to do with your competition. Your ability to retain and engage employees not only makes you a more attractive place to work, but it also makes your teams more productive.

That retention and engagement can give your organization a significant competitive advantage over its competition. Unfortunately, many businesses struggle to overcome the challenge of regrettable attrition and aren’t able to experience that advantage. Lauber Business Partners team of consultants can help your organization’s managers overcome the challenges that drive regrettable attrition. To learn more about our manager training and HR consulting on employee engagement, get in touch with our team today!

What is Team Culture?Most definitions of team culture are vague statements that conjure a general sense of positivity. They say things like, ‘team culture refers to the shared values, norms, attitudes, and beliefs that shape the collective identity of individuals within a team.’ That’s not very helpful, is it? Let’s cut the abstractions and jargon and put it simply. Team culture is the way people treat each other at work, what people think and feel about their work, and how they perform their work. Team culture is to a business as a cyclist is to a bike; you can have the best setup tuned to perfection, but without anyone to give it power and direction, it’s not going anywhere. What ISN’T Team Culture?Perks aren’t culture. Perks might determine what employees encounter when they show up to work, but culture influences the way people feel and how they act when they show up to work. Perks often get confused with team culture because for decades, growth-driven businesses failed to devote resources to anything that wasn’t obviously driving results. But then these businesses full of high-performing professionals started noticing that their teams were burning out. When these businesses finally came to the realization that the pressure was actually holding their teams back, their knee-jerk reaction was to make employees more relaxed and comfortable at work. Soon, the world saw a wave of corporate game rooms, slides, and nap-pods flood across their LinkedIn feeds and the pages of business journals. But these perks missed the mark, and the ping-pong tables went unused. Why? Because the perks didn’t actually change the way teams communicated, gave feedback, or collaborated. They didn’t change the culture. Here’s How Building a Team Culture Impacts the Bottom LineTeam culture is largely invisible, but its impact isn’t. Team culture has direct and measurable impacts on organizations. 1. Healthy Team Cultures Make Businesses More ProfitableAccording to a report from McKinsey, organizations with a strong culture are more profitable. The businesses with the best team cultures are delivering 60% more profits to their shareholders than businesses with average team cultures, and 200% more than those with the worst cultures. Additionally, team culture engages employees, and that’s one of the most valuable things a business can do. How valuable? Engaged teams can see a nearly 20% increase in productivity, while teams with disengaged employees can damage productivity by as much as 40%. 2. A Healthy Team Culture Makes Your Business AdaptableChange can be a challenge, but healthy team cultures can adapt and work through it. A team culture built on healthy and efficient communication, shared goals, trust, and genuine buy-in can shift directions faster than a team culture that’s fragmented. When a healthy team culture exists in an organization, employees feel comfortable and empowered to share their thoughts and concerns openly. When a team has that level of trust and confidence in their colleagues, it allows them to share information rapidly, accelerating the rate at which they adapt. 3. Team Culture Helps Your Business Retain TalentLosing key employees hurts your bottom line big time. According to SHRM, the cost of replacing a talented colleague can be three to four times their annual salary. That means that in industries with stiff competition, a healthy team culture can ultimately be the key differentiator that gives your business an advantage. If you want to avoid an uncomfortable conversation about recruitment costs in your next quarterly budget meeting, focus on engaging your teams. When your team culture is engaging and healthy, employees are almost 90% less likely to leave. How to Build a Team CultureBuilding team culture isn’t a one-time thing. In fact, it’s never finished. But that doesn’t mean building a team culture is a Sisyphean task; rather, think of team culture like an organism. You need to take the time to raise it, and you need to care for it throughout its life.

If you’re an HR pro or a People Manager struggling to build or maintain a healthy team culture, know that you’re not alone. As remote work becomes increasingly common and employee expectations continue to change, trying to keep a pulse on the numerous factors that impact team culture and engagement is only getting harder. We’re here to help. Lauber Business Partner’s consulting on employee engagement can help businesses like yours identify roadblocks and develop a strategy for moving past them. If you’re ready to make work better, get in touch with Lauber Business Partners today.  Employee retention is vital, but why should you invest in it? The short answer is: because you can’t afford not to. The longer answer requires a look at attrition—the alternative that faces your business. What’s the True Cost of Attrition?Attrition has hard costs like hiring expenses, which can grow quickly, but there are also other impacts that are harder to measure. So how does attrition truly affect your business? Attrition Impacts Employee MotivationWork friendships are real and they matter, not just to your employees, but to your business’ productivity. If two employees are close and one leaves, it can leave the other feeling less motivated. It could even lead them to start looking for new opportunities, further increasing your attrition rate. Attrition Impacts MoraleWhen employee churn is high at your organization, it sends the wrong message to current and new employees. For new hires, it hints that they’re in a company where their career won’t grow. Why would they want to stick around there? For veteran employees and managers, attrition can lead to a frustration and an increasing workload when they have to pick up extra work and recruit a new employee. Attrition is the Enemy of ProductivityWhen an employee leaves, their responsibilities don’t leave with them. Someone has to pick up that slack, and that can lead to poorer performance for the business. Additionally, attrition means your business is losing institutional knowledge that’s been developed over years. You may be able to replace an employee in three months, but you’re not guaranteed to regain that knowledge with a new hire. Effective teams create productivity by blending different skills and abilities into a single mechanism. In short, effective teams create exponential impact, not additive impact. The risk here is that the removal of even one key component stifles the output of the entire team in a similarly exponential fashion. So what do you need to do to limit attrition and improve employee retention? Building a Smart and Healthy Culture Can Improve Employee RetentionLeaders and managers have a serious need to solve the problems that attrition poses. Easier said than done. There’s also no single solution. Each business faces unique challenges and needs custom solutions. However, those solutions begin at the top with managers and leaders. The decisions, actions, and attitudes of the people in these positions will percolate through the organization, for better or for worse. To reap the benefits of employee retention, get focused on these key areas: 1. Develop Your LeadersIf there was a singular answer to the question “why does attrition happen?” it would be ‘managers.’ According to a study from Gallup, managers are largely responsible for disengaged teams. These are the same teams that are prone to attrition and low productivity. However, saying “managers are failing” doesn’t fix things, and it’s also not totally accurate. The truth is that most managers don’t have the skills and tools they need to cultivate successful teams. Just like new hires need training and opportunities for ongoing development, so do managers. To improve retention in your business, you need to address the reason so many employees leave. That reason is often managers. Invest in coaching and professional development for managers and teams. When that happens, things downstream of your managers, like employee retention, can turn around. 2. Build Effective TeamsThe success of every business depends on the performance of its teams – leadership teams, departmental teams, shop floor teams and project teams, among many. Patrick Lencioni, the author of many management books, including The Five Dysfunctions of a Team, says, "If you get all the people in an organization rowing in the same direction, you could dominate any industry, in any market, against any competition, at any time." Because of the unique make-up of individuals, no teams are identical. It is crucial that team members understand one another and how to work effectively with one another. It is also crucial to understand what team expectations are and what it means to be a great team member. Team members are interdependent and investing in the health of your teams is an investment that pays big dividends. No business can reach its potential without effective teams. 3. Communicate Effectively and Build TrustEffective communication is foundational for the success of any team. You’ve heard it a million times. But what does this actually look like?

These efforts build trust. When trust is established, teams are better off for many reasons. For example:

4. Follow ThroughOngoing development opportunities and open communication are vital for improving employee retention, but they’re not one-time quick fixes. They require maintenance, time, and dedication. When leaders and teams have good communication, things run smoothly, conflict is resolved efficiently, and productivity soars. But you have to keep at it—even when employees inevitably do leave. The Benefits of Employee Retention are Within ReachBusinesses are like cars. Hit the gas all you want, but without someone steering, you’re going to crash. Smart and healthy business cultures understand the need to prioritize both in order to reach their business goals.

By coaching and developing managers, building effective teams, communicating effectively and building trust, and being consistent at this, your business can make significant strides toward retaining employees and building a smart and healthy organization. Your bottom line—and your employees—will thank you. The benefits of employee retention are yours for the taking, but it’s not always easy to find the areas that need attention. If your organization is struggling with employee retention or wants to turn your employee engagement into a strategic strength, get in touch with the team at Lauber Business Partners. Our team can perform an engagement assessment to help your organization make strides toward becoming smart and healthy.  For many small and mid-sized businesses, hiring a full-time Chief Financial Officer (CFO) can be a major expense that simply isn't feasible. Fortunately, there is a solution that allows businesses to access the expertise of a CFO without the high costs associated with a full-time position. That solution is a fractional CFO. A fractional CFO is a financial expert who works part-time for a business, providing strategic financial guidance and support as needed. This can be a cost-effective solution for businesses that need help managing their finances but don't require or cannot afford a full-time CFO. Here are some of the benefits of a fractional CFO:

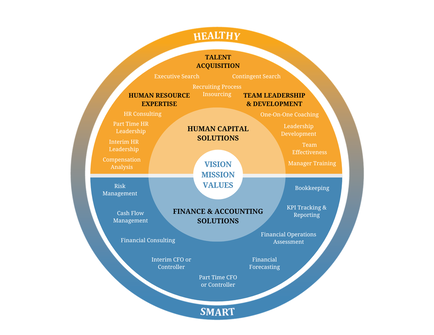

By providing expert financial guidance and support, a fractional CFO can help businesses make better financial decisions, reduce costs, and increase revenue. This can improve profitability, cash flow, and overall financial health. In conclusion, a fractional CFO can be a valuable asset for small and mid-sized businesses. They provide access to financial expertise, flexibility, cost savings, an objective perspective, improved financial performance, and a partner in strategic decision-making. If you're looking for a cost-effective way to manage your finances and move your business forward, consider hiring a fractional CFO. Engage a seasoned Lauber Fractional CFO with extensive skills, experience, and strategic insight without paying for a full-time resource. With the Fractional model, you can engage a CFO on a flexible part-time basis—a day or two a week, once a month, or as often as needed—at a cost you can afford. You can rest comfortably knowing that a Lauber Fractional CFO is proficient in the most complex Finance and Accounting topics. At Lauber, we don’t treat organizational health as an afterthought. To us, it’s essential. So, alongside the services we provide our clients to help them build and maintain the smart parts of their businesses (like Finance and Accounting and HR services), we offer innovative menu-based leadership and development programs and talent acquisition services, resulting in a healthy and positive team culture that drives results. WHAT DOES IT TAKE TO BE A SMART AND HEALTHY COMPANY?  In today's fast-paced and competitive business environment, the success of an organization depends not only on its profitability but also on its ability to create a healthy and sustainable workplace. The concept of a smart and healthy organization is gaining traction as organizations realize the benefits of prioritizing employee well-being and creating an environment that fosters innovation, creativity, and collaboration. This blog will discuss what it means to be a smart and healthy organization, and the steps organizations can take to become one. What is a Smart and Healthy Organization?A smart organization is one that has expertise in traditional areas like strategy, finance and accounting, operations, engineering/design, marketing, sales, and human resources. A smart and healthy organization also prioritizes employee well-being and creates an environment that promotes physical, emotional, and intellectual health. A smart and healthy organization is one that invests in its employees by providing them with the necessary resources and support to thrive both personally and professionally. Such an organization recognizes the importance of maintaining a healthy work-life balance and encourages its employees to care for themselves. Characteristics of a Healthy OrganizationA smart and healthy organization exhibits the following characteristics:

The Benefits of a Smart and Healthy OrganizationOrganizations prioritizing employee well-being and creating a healthy workplace enjoy several benefits. These include:

Stay Smart and Get Healthy with Lauber Business PartnersIn conclusion, creating a smart and healthy organization requires a commitment to employee well-being, a positive work culture, innovation, and creativity, learning and development, and sustainability. By prioritizing these areas, organizations can create a workplace that promotes employee well-being, fosters innovation, and enhances the organization's reputation, leading to increased productivity and engagement, lower turnover rates, and improved employee health.

At Lauber, we don’t treat organizational health as an afterthought. To us, it’s essential. So, alongside the services we provide our clients to help them build and maintain the smart parts of their businesses we also offer an innovative menu-based leadership and development program, elegantly layered organizational health curriculum with integrated coaching, to create a healthy and positive team culture that drives results. What does it take for an organization to be smart and healthy? And why is it more important than ever to create workplaces where employees know that their leaders not only recognize and appreciate their unique talents, but also genuinely care about their well-being? Patrick Lencioni, the author of the best-selling business book The Advantage, makes a convincing case that the most successful organizations don’t just master strategy, marketing, and finance and accounting, the traditional “smart” facets of business operation; they also consciously build positive, healthy cultures in their organizations. When leaders take clear steps to reduce office politics and confusion, and help their employees find what brings them joy and energy at work—creating the conditions of trust and vulnerability that promote organizational health—the payoffs are profound, Lencioni explains. From a practical standpoint, businesses that prioritize health have a strong strategic advantage, because their employees are more productive and engaged. Their employees are also less likely to leave the organization, taking critical knowledge with them—another huge gain in this age of the great reshuffling, when a record number of Americans are quitting their jobs to find work that’s more fulfilling. Organizational health also creates positive ripple effects that improve employees’ relationships with clients and customers, and even their own families and communities. When people go to work with “clarity, hope, and anticipation,” and come home with “a greater sense of accomplishment, contribution, and self-esteem,” the impact, per Lencioni, “is as important as it is impossible to measure.” At Lauber, we don’t treat organizational health as an afterthought. To us, it’s essential. So, alongside the services we provide our clients to help them build and maintain the smart parts of their businesses—including support for finance and accounting, human resources, and strategy—we also offer an innovative menu-based program, rooted in Lencioni’s elegantly layered organizational health curriculum with integrated coaching, to create a healthy and positive team culture that drives results.  THE LAUBER MODEL FOR ORGANIZATIONAL HEALTHAs we emerge from the pandemic, we’re hearing from leaders who are eager to make health the prevailing cultural value in their organizations going forward. Some want focused support to reboot and refresh by helping their employees reconnect with each other, plus the parts of their work where they excel. Some want to break down silos that have long contributed to inefficient decision-making, and distrust, in their companies. And others, doing team development for the first time, want to do a deep dive, instilling healthy practices into every aspect of their operations. If you would like to make your organization healthier, here are some of the ways we can help:  Specific to the healthy initiatives, we’ll work with you to design a coaching program and bring it to life. It could include a Team Culture Assessment to identify your organization’s collective strengths and challenges, or a Working Genius Assessment to help individuals and teams find their natural gifts for certain tasks, or both. And if a deep dive is in order, we can also work with you and individuals across your organization—with a combination of one-on-one coaching and facilitated team sessions—to build trust, master the art of healthy conflict, achieve commitment, and embrace accountability. Contact Lauber Business Partners TodayWe’re proud that our healthy culture coaching consistently improves interpersonal dynamics, enhances team performance, and fosters individual growth—delivering triple-impact results that help businesses thrive.

To learn more, contact us at info@lauber-partners.com.  What does it take for an organization to be smart and healthy? And why is it more important than ever to create workplaces where employees know that their leaders not only recognize and appreciate their unique talents, but also genuinely care about their well-being? Those of you who were able to join us last week for “The Power of Organizational Health and Clarity,” a livestreamed talk by management consultant Patrick Lencioni, will already have some answers to these timely questions. Lencioni, author of the best-selling business book The Advantage, made a convincing case that the most successful organizations don’t just master strategy, marketing, and finance and accounting, the traditional “smart” facets of business operation; they also consciously build positive, healthy cultures in their organizations. Organizational HealthWhen leaders take clear steps to reduce office politics and confusion, and help their employees find what brings them joy and energy at work—creating the conditions of trust and vulnerability that promote organizational health—the payoffs are profound, Lencioni explained. From a practical standpoint, businesses that prioritize health have a strong strategic advantage, because their employees are more productive and engaged. Their employees are also less likely to leave the organization, taking critical knowledge with them—another huge gain in this age of the great reshuffling, when a record number of Americans are quitting their jobs to find work that’s more fulfilling. But going beyond the office, organizational health also creates positive ripple effects that improve employees’ relationships with clients and customers, and even their own families and communities. When people go to work with “clarity, hope, and anticipation,” and come home with “a greater sense of accomplishment, contribution, and self-esteem,” the impact, per Lencioni, “is as important as it is impossible to measure.” Improving and Maintaining Organizational HealthAt Lauber, we don’t treat organizational health as an afterthought. To us, it’s essential. So, alongside the services we provide our clients to help them build and maintain the smart parts of their businesses—including support for finance and accounting, human resources, and strategy—we also offer an innovative menu-based program, rooted in Lencioni’s elegantly layered organizational health curriculum with integrated coaching, to create a healthy and positive team culture that drives results. As we emerge from the pandemic, we’re hearing from leaders who are eager to make health the prevailing cultural value in their organizations going forward. Some want focused support to reboot and refresh by helping their employees reconnect with each other, plus the parts of their work where they excel. Some want to break down silos that have long contributed to inefficient decision-making, and distrust, in their companies. And others, doing team development for the first time, want to do a deep dive, instilling healthy practices into every aspect of their operations. CONTACT Lauber’s Organizational Health-Focused CoachingIf you would like to make your organization healthier, we can help you, too. We’ll work with you to design a coaching program and bring it to life. It could include a Team Culture Assessment to identify your organization’s collective strengths and challenges, or a Working Genius Assessment to help individuals and teams find their natural gifts for certain tasks, or both. And if a deep dive is in order, we can also work with you and individuals across your organization—with a combination of one-on-one coaching and facilitated team sessions—to build trust, master the art of healthy conflict, achieve commitment, and embrace accountability.

We’re proud that our healthy culture coaching consistently improves interpersonal dynamics, enhances team performance, and fosters individual growth—delivering triple-impact results that help businesses thrive. To learn more, please feel free to contact us. We'd be happy to discuss your organization’s needs and help you design your own roadmap to results. Please contact us by email at info@lauber-partners.com or by phone at 414-273-8060.  Every day there is news about the stock market's heavy hitters. GOOG, FB, TSLA and other big-ticket ticker symbols float across the bottom of news broadcasts. However, the vast majority of U.S. companies are privately held. So, if privately held companies can’t issue public stocks, how do they raise money? Many companies bootstrap themselves with owner or family and friends equity or loans to start. Two other vehicles for raising funds are private equity and venture capital. Here, we'll discuss what each does, how they're different and similar, and why the private market remains so resilient and attractive to businesses and investors. What's the difference between private equity and venture capital?Let’s explore the main differences between private equity (PE) and venture capital (VC) firms: Venture CapitalVenture capital firms raise funds by gathering investments from limited partners (LPs), whose money they then invest. VC firms are known for focusing their investments on startups and other young companies that show high potential for growth and above average rates of investment return. Often these companies are characterized by innovation or carving out a new industry niche. Frequently, they involve some new technology or other innovation. As such, VC investments are normally much riskier than Private equity investments but also have potentially higher returns. The role a venture capital firm takes following their investment frequently includes a Board of Directors seat and, consequently, significant input into its future direction. They can also attract other investors and provide valuable connections for the company to expand their business. Because of the amount of capital sometimes involved in these investments, numerous VC firms may invest in a given entity. As such, a single firm does not often have a controlling interest in the company. Also, sometimes, the founders maintain control by having special stock voting rights or control provisions that allow them to maintain control of the company. Private Equity One of the most significant ways private equity differs from venture capital is in the type of companies in which they invest. Whereas venture capital primarily funds startups as they grow and blossom, private equity often invests in more established operating companies with opportunity for growth or improvement. Private equity firms raise capital from institutional investors and wealthy individuals, often in a fund. The fund or firm normally takes controlling interests in these more mature operating companies. The investment of their equity is almost always coupled with debt, sometimes quite significant, to fund the company purchase price. In some instances the prior owner of the acquired entity will also continue to hold some equity in the new entity. They then seek to improve the company via additional growth opportunities (new products, new services, add-on acquisitions, geographic growth, enhanced sales and marketing capabilities, etc…) or operating improvements (cost reductions, improved technology, improved operating processes, etc…), leading to enhanced shareholder value. In accordance with its majority equity stake, the PE firm normally controls the Board of Directors of the acquired entity. This gives them control over the management team and strategy of the acquired entity. PayoffOne of the fundamental similarities between private equity and venture capital firms is that they both aim to achieve the same thing: leveraging their existing capital, resources, and knowledge to make businesses more profitable and more valuable. They get their payoff in similar ways too – normally from a sale or merger of the acquired company with another entity. This could be an outright sale to another party, merger with another entity or a sale via an initial public offering. Upon such an event the VC or PE firm achieves a return, which is ultimately passed along to its investors. Why Is There So Much Interest in Venture Capital and Private Equity?One of the primary reasons so much capital is flowing into venture capital and private equity is that yields on other investments have declined in recent years. Investments in treasury bills and other debt securities have extremely low returns due to the low interest rate environment that has been in place for the last decade. Additionally, there is a wave of baby boomer owned companies that have no transition plan and are being sold. Private Equity firms are often great buyers for these companies, with ready capital and an infrastructure to manage the purchased entities. Lauber’s Business Expertise Regardless of what funding avenue your business chooses to pursue, you're going to experience a fundamental shift in the way your business operates. Startups that have been bootstrapped until their funding will suddenly be able to hire more employees, specialize their business operations, and scale upward. More mature businesses might need to change their organizational structure, operating procedures, personnel, financing facilities and other things as they pursue new growth. Navigating these times is critical to the future success of your organization, and Lauber’s Finance & Accounting, Human Resources, Talent Search, Coaching and Planning services will provide you with the expertise you need to take your business to the next level. . A Lauber Fractional leader proficient in the most complex. Lauber delivers its services fractionally (i.e., a day-a-week or on some other regular schedule), on an interim basis or a project consulting basis. Contact Lauber Business Partners for Fractional, Interim or Project Consulting Leadership Today.At Lauber Business Partners, we understand what it takes to deliver exceptional expertise that will significantly impact your organization’s success. Please contact us by email at info@lauber-partners.com or by phone at 414-273-8060.

As the landscape of business continues to grow and change, one thing is more true than ever: talent is king. The recruiting strategy employed by your organization is of utmost importance when it comes to putting your business on the path to success and growth. Though it may fly in the face of preconceived notions of recruitment, the recruiting process is best implemented as an ongoing strategy. Why An Ongoing Recruiting Strategy is Best Continuous recruiting is accompanied by several benefits, especially compared to a more sporadic and temporary recruitment process: 1. Gives You Constant Surveillance Utilizing modern ongoing recruitment strategy and process provides your organization with a constant view of the market for talent. 2. Identifies Talent as It Becomes Available Finding the right fit for your company is all about timing: whether it’s timing of the applicant or timing of the job market and economy. Utilizing an ongoing recruiting strategy means your hiring process will be dialed in and ready to capitalize on the right candidate at the right time. 3. Actively Builds Your Brand in the Marketplace Proactively recruiting also gives your organization the consistent platform to be seen, allowing your brand to be seen and engaged by prospective employees. 4. Enables You to Move Quickly Position vacancies take a serious toll on your organization’s ability to operate, and depending on your size and industry, can be devastating. An ongoing recruitment process allows you to fast track and prioritize certain vacancies. Ongoing Recruiting with lauber business partnersRecruitment through Lauber is more than a service. We’ll work with your business as an extension of your team, ensuring that we are fully aligned with your goals and requirements as you build your ideal team. Working closely like this allows us to gain intimate knowledge of your company culture and needs, aligning ourselves with your priorities. We offer multiple models that we can tailor to your specifics: Recruitment Process Insourcing (RPI) RPI is a scalable and flexible model that allows for a dedicated recruiter to work only with your team and your positions. This recruiter works as an extension of your organization, fully representing you in the candidate field. You’ll have access to the data and recruitment tools, and you’ll only be charged a flat monthly fee. Contingent Search Lauber’s Contingent Search model is best utilized when recruiting for hard-to-find professionals; candidates who are the best long-term fit for your company. This model is paid for through a contingent fee and allows your own team and resource to be freed up while we take on the searching and vetting process. Lauber offers two kinds of contingent search: Executive Search to deliver top-level management and c-suite candidates and Non-Executive search for independent director and supervisor roles. Interim Staffing When your organization is in need of candidates for specific projects or general short term needs, Lauber’s interim consulting resources bring experienced personnel that can hit the ground running. Contact Lauber Business Partners for REcruiting ServicesAt Lauber Business Partners, we understand what it takes to deliver exceptional candidates that will significantly impact your organization’s growth. If you want to learn more about how your organization could benefit from Lauber’s ongoing recruiting and interim staffing models, please contact us by email at info@lauber-partners.com or by phone at 414-273-8060. Additional Resources |

RSS Feed

RSS Feed

|

|

Website by RyTech, LLC